UK wage growth remains sticky despite cooling jobs market

UK wage growth appears stuck in the 4.5-5% area, despite falling private sector employment and lower vacancy rates. Further declines in wage growth are coming, but not immediately. For the time being, the Bank of England will remain cautious.

There’s one number that will catch the UK’s headlines this morning, and that’s the surprise surge in the unemployment rate from 4.0% to 4.3%. That’s a sizable rise and much bigger than anyone had anticipated. It’s also unusual because this number is based on three-month moving averages, which tends to dampen the volatility in this data.

In reality, of course, this tells us very little. The Office for National Statistics readily concedes that these figures suffer from well-known reliability problems. Indeed, all this rise really does is reverse an equally strange dip in the unemployment rate from earlier in the summer.

That’s not to say the jobs market isn’t cooling – it undoubtedly is. With one or two notable exceptions, the vacancy rate in the majority of sectors is comfortably below pre-Covid levels. If we look at internationally comparable data from Indeed, the hiring agency, this isn’t a trend that’s been repeated so far – at least not as dramatically – in the US, Germany or France.

UK vacancy rates are generally below pre-Covid levels

Source: Macrobond, ING calculations

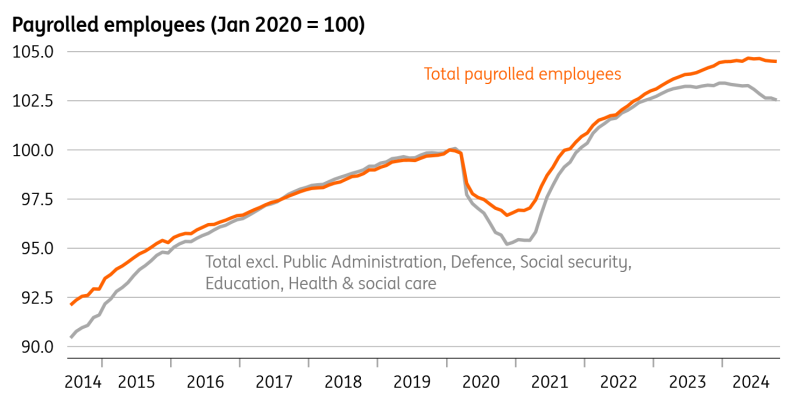

It’s a similar story with data taken from firms’ payrolls. Strip out sectors with a high concentration of public sector roles, and the number of payrolled employees has fallen by 0.8%, or 160,000, since the turn of the year.

These aren’t huge numbers, nor do these represent rapid changes in trend or the classic signs of recession. Redundancy levels are still very contained, for instance.

Still, against that backdrop, it’s surprising that wage growth is still as strong as it is. Private sector wage growth is close to 5% year-on-year. That measure is likely to tick higher over the next few months due to unfavourable base effects. Even if we look at more timely measures of wage growth, like the change compared to three months ago, these are still consistent with annual rates of roughly 4.5%. The Bank of England’s ‘Decision Maker’ survey of corporates has also seen the expected level of wage growth level out at around 4%. We think it’ll take until the second quarter of next year for the official private sector wage growth numbers to fall below that level.

Excluding government-heavy sectors, payrolled employment has fallen this year

Source: Macrobond, ING calculations

What does this all mean for the Bank of England? Given how far the jobs market has cooled, there’s nothing here that should stop officials from cutting rates to a much more neutral position. To our mind, that means rates in the 3-3.5% area. Markets are pricing fewer than three rate cuts now over the next two years, which we think is too little.

For now, though, both wage growth and services inflation are likely to remain sticky into year-end and early next year. Barring any surprises, we think the Bank will stay cautious and keep rates on hold in December, before cutting again in February. Assuming the data looks a little better by then, we think rate cuts will accelerate thereafter.

Read the original analysis: UK wage growth remains sticky despite cooling jobs market

Related

Llyods Recruiting Engineers In India After Slashing Jobs In UK

Lloyds Banking Group is planning to hire hundreds of engineers in India as the company plans to shift its employment opportunit

Major new funding for music acts that supercharged careers of…

£1.6m Music Export Growth Scheme to support 58 independent UK artists to tour the world Funding will boost UK’s creative industries – a key growth se

Well-loved restaurant chain to close 8 venues across UK as…

A BELOVED restaurant chain has announced it will close eight venues across the UK, scrapping 158 jobs in the process.Owners are pointing the finger at Labour's

US adds 151,000 jobs in February as unemployment rate ticks…

The latest figures published by the US Bureau of Labor Statistics today (7 March) came in below market expectations, with economists polled by